How Engagement is Reshaping Video Game Platforms

Evidence from Microsoft's Xbox reveals that drivers of user engagement for both video games and consoles are not the same as the traditional drivers of sales.

Platform Papers is a blog about platform competition and Big Tech. Prominent academics discuss their latest research. The blog is linked to platformpapers.com, a repository that collects and organizes academic research on platform competition.

In June 2017, Microsoft made a bet that many in the gaming industry considered risky. Rather than doubling down on selling hardware and software titles (the revenue model that sustained the console video game industry for decades), Xbox launched Game Pass, a subscription service offering access to a rotating library of hundreds of games for a monthly fee. Five years later, Sony followed with a revamped PlayStation Plus. Today, these subscription services have become central to how both platforms compete for players.

But what does the shift from selling games to retaining players mean for the broader platform ecosystem? And did the bet pay off? Two new studies examine these questions from complementary angles: one focused on how engagement differs fundamentally from sales when it comes to measuring platform and software success, and the other on whether subscription models actually help or hurt platform and software revenues.

“Once a console or game is purchased, sales figures go silent. They cannot reveal whether consumers continue to use the platform and software they bought, or quietly abandon them.”

Why Engagement Is a Different Game

The marketing and economics literatures have long relied on sales data to study platform and software success in platform markets like the video game console industry. Yet these markets have fundamentally changed. Ahead of Microsoft’s latest console launch, its then-CEO of Gaming Phil Spencer declared: “Our strategy does not revolve around how many Xboxes I sell this year. […] for us, it’s about engagement.”, pivoting to “engagement metrics rather than device metrics” to measure software and platform success. Firms focus on engagement because their business models depend on engagement; both software sellers as well as platform owners increasingly rely on subscription services to commercialize their software and platforms. But subscription services are engagement platforms, not sales platforms. Understanding the drivers of engagement is therefore crucial. This is where sales data fall short.

Once a console or game is purchased, sales figures go silent. They cannot reveal whether consumers continue to use the platform and software they bought, or quietly abandon them. Consumers can vary their usage, switch between titles, or disadopt platforms and software entirely, and none of this shows up in sales.

Our study, published in the Journal of the Academy of Marketing Science, uses engagement data to study the console market directly. Using a panel of over 14,000 Xbox users between 2020 and 2022, we tracked both daily engagement (i.e., the number of active users) and monthly sales for over 2,700 game titles and the Xbox consoles they were played on. This allows, for the first time, a direct comparison of sales and engagement in a platform market.

“Characteristics that have traditionally dominated what drives software and console success, such as superstar titles (with high review scores), exclusive games, and new intellectual properties (IP), decline sharply in relative importance when it comes to engagement.”

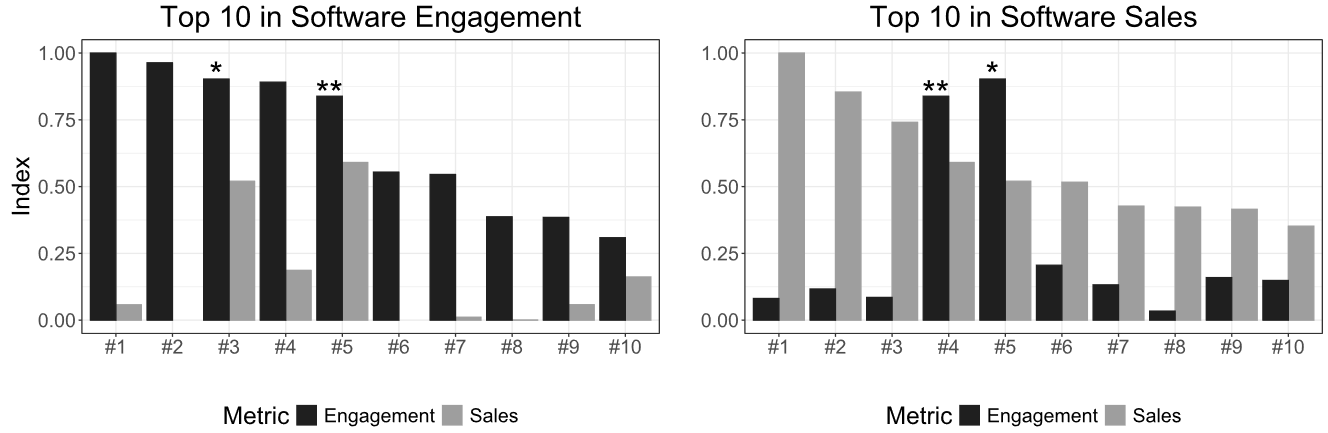

The difference is noticeable. The figure below illustrates that, on Microsoft’s Xbox platform, out of the top 10 most engaging video games of 2021, only 2 appear within the top 10 most sold. Likewise, most top selling titles display disproportionally little engagement. When the most engaging titles are so clearly different from the most purchased ones, it calls into question whether the established drivers of platform and software success still hold when considering engagement instead of sales.

“Non-superstars, franchises, and games available on multiple platforms all become much more important for engagement than they are for sales.”

They do not. We find that the drivers of engagement are fundamentally different from the drivers of sales. Characteristics that have traditionally dominated what drives software and console success, such as superstar titles (with high review scores), exclusive games, and new intellectual properties (IP), decline sharply in relative importance when it comes to engagement. Without the pre-purchase information search that typically boosts their sales (reviews, trailers, consumer hype), these titles lose much of their advantage in the faster-paced decision of choosing what to play compared to what to buy. Superstar games, for instance, sell about ten times more than non-superstars. In engagement, that gap narrows to less than twofold. The same holds for platform sales. For each 100 consoles that previous research finds are sold due to a superstar release, we find that at most 37 users become active on theirs.

What matters instead? Non-superstars, franchises, and games available on multiple platforms all become much more important for engagement than they are for sales. Especially when those games are available on the platform’s subscription service, such as Game Pass. Being featured in the Game Pass catalogue is the single most powerful driver of engagement.

We attribute this to a valuation-usage disparity. Buying a game is a one-time, high-stakes commitment where consumers rely on quality signals before spending $60 or more. Choosing what to play on a given evening is fundamentally different: faster, lower-stakes, and repeated daily in a market far more crowded than the market for what to buy. In this context, consumers seek variety over quality, which is why non-superstars and multiplatform games gain ground. Consumers also regress to what is familiar, returning to known franchises that do not require the information search or learning curve of new IPs. Because subscription services cater to both impulses, this makes them a uniquely powerful engine of engagement.

“Unlike in music and film, gaming subscriptions did not significantly cannibalize platforms’ software revenue in the aggregate.”

Are Subscriptions Commercially Sustainable?

If subscriptions are this powerful at driving engagement, the natural follow-up question is whether they are commercially sustainable. When subscription models entered the music and film industries, they cannibalized existing revenue streams. Would the same not happen in gaming?

A second study, published in the International Journal of Research in Marketing, provides early evidence that gaming is different. Using industry data around the launches of Xbox Game Pass in 2017 and the revamped PlayStation Plus in 2022, we examined the commercial consequences of the introduction of subscription services to the console market. Four findings stand out.

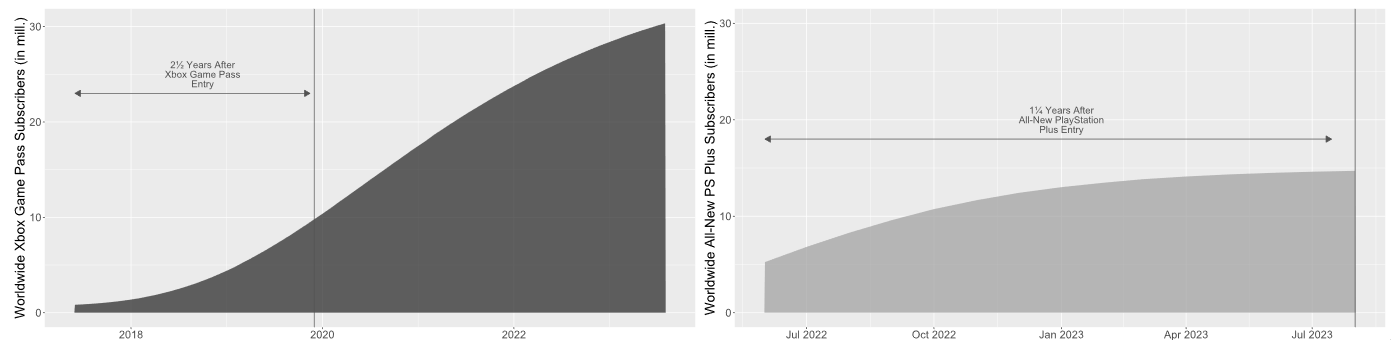

First, both major subscription models under study generated an enormous stream of subscription revenue for their platforms since launch. Neither Microsoft nor Sony comment regularly on their subscriber numbers, but both are estimated to reach millions of users monthly, leading to billions in additional revenue (see figures below).

Second, both platforms actually saw increased rather than decreased hardware revenues following their subscription launches (compared to if they would not have done so). This may be because consumers who know they will have access to a large library of games have a stronger reason to invest in the hardware and to stay within the ecosystem because of the subscription service’s cost-effectiveness and convenience.

Third, the impact on video game sales revenue was limited. Unlike in music and film, gaming subscriptions did not significantly cannibalize platforms’ software revenue in the aggregate. A likely explanation is that, contrary to Spotify or Netflix, video game subscription services still integrate a storefront: any content discovered on the subscription can be bought seamlessly for perpetual ownership. The service also incentivizes purchasing additional content such as expansions, sequels, or other entries in the franchise or genre. These benefits seemingly outweigh any sales cannibalization.

Finally, subscriptions were associated with a healthier supply of new games, though the mechanism differed across platforms. For PlayStation, subscription introduction coincided with more new releases. For Xbox, the effect appeared in quality, with higher average review scores after Game Pass launched. Subscriptions likely provide developers with a more predictable revenue stream and guaranteed distribution, reducing the all-or-nothing risk of depending on launch-week sales, which incentivizes a healthier software supply.

About the research: The first study uses daily engagement data from 14,000+ Xbox users (2020–2022) to compare drivers of sales versus engagement across 2,700+ video game titles, finding that traditional drivers of platform and software success, i.e., superstars, new IPs, and exclusives, decreased in relative importance, while non-superstars, franchises, and multihomed software (especially on subscription services) play a substantially bigger role in engagement than they did in sales. The second study provides first evidence of the commercial consequences of Xbox Game Pass (2017) and PlayStation Plus (2022) on the console market, finding that subscriptions enhanced console revenue, had limited impact on game sales revenue (contrary to cannibalizing effects in music and film) and created a healthier supply of new game titles.

What It Means for the Platform Economy

Taken together, these two studies paint a coherent picture. The shift toward engagement-based, subscription-driven business models in the video game industry is not just commercially viable, it is reshaping the drivers of success.

For platform owners and software developers, sales metrics alone no longer capture where value is created. Engagement data reveal a fundamentally different competitive landscape, one where content breadth, familiarity, and subscription accessibility matter more than ever before. Superstar quality still drives success, but much less than expected based on sales. Subscriptions also create new opportunities: titles that struggle at retail can find sustained audiences through subscription libraries. Particularly franchises and non-superstar games thrive when players are choosing what to play from a subscription catalog rather than what to buy.

These findings may help appease video game developers that have questioned whether the subscription and/or engagement model makes sense for their industry, fearing the financial uncertainty and cannibalization associated with. If anything, these models have democratized the landscape: platforms and developers should not necessarily obsess over releasing superstar quality, new IPs or achieving exclusivity deals, which anecdotally have been increasingly hard to attain and take up unsustainable amounts of time and costs. Non-superstars and multihomed titles matter too, and provide enough richness in the customer experience to draw consumers in. This is especially true when released in subscription catalogs, which itself needs not necessarily hurt their sales.

This blog is based on research published in the Journal of the Academy of Marketing Science and the International Journal of Research in Marketing and is included in the Platform Papers references dashboard:

Van Crombrugge, M., & Stremersch, S. (2025). Engagement in platform markets: A (video) game changer? Journal of the Academy of Marketing Science, 53(5), 1422-1446.

Van Crombrugge, M., & Stremersch, S. (2025). The rise of the subscription model in the video game console industry: Unveiling the commercial consequences for platform owners and video game sellers. International Journal of Research in Marketing.

Platform Leaders Academic Prize - Finalists Announced!

Each year, Platform Leaders awards a prize to an academic paper that demonstrates exceptional relevance and practical applications to the business world. Finalists are selected in partnership with platformpapers.com.

We are excited to announce the Finalists for 2026:

Antitrust platform regulation and entrepreneurship (Rong, Sokol, Zhou, and Zhu)

Growing platforms by adding complementors without a contract (Mayya and Li)

The Price of Platform Participation (Zhu, Shi, and Banerjee)

The winner is selected by a business jury. Platform Leaders invites the author(s) to present the paper’s key findings at its annual conference in November, and also commissions an animated video abstract highlighting the research’s key ideas.

Prior winners include Manav Raj for his work on Demand Spillovers and Competition in the context of music streaming platforms and Joe Ploog and Joost Rietveld for their work on Heterogeneous Network Effects in the board games industry.

Platform Updates

Apple showcases new Apple Intelligence and a Siri revamp (📑): Apple’s WWDC will reportedly unveil a Gemini-powered Siri overhaul alongside a new AI agent App Store. By outsourcing its foundational model, Apple aims to ensure its proprietary physical devices remain the ultimate driver of ecosystem lock-in.

YouTube bypasses textbook gatekeepers to capture American schools (🔈): The video platform has become an essential classroom tool, creating a shadow educational hub that sidelines traditional textbook publishers. By leveraging its massive free library, Google secures early ecosystem lock-in among younger students, protecting it against rival media platforms.

Meta pivots to enterprise AI with automated business agents (📑): Meta has launched an AI assistant across WhatsApp and Messenger to handle customer service for companies. Shifting to a usage-based software fee helps Meta expand beyond its traditional advertising revenue and lock corporate clients into its network.

Spotify integrates generative AI into podcasts and audiobooks (📄): The streaming giant is launching conversational chatbots and personalized AI-generated audio directly within its platform. By providing instant contextual answers so listeners never have to leave, Spotify aims to defend its multi-sided audio platform from external search engines.

EU unveils Tech Sovereignty package to bypass foreign gatekeepers (📑): The European Commission launched sweeping legislation to secure independent control over its data and digital infrastructure. By curbing an 80% reliance on foreign tech providers, the bloc aims to build a self-sustaining continental ecosystem.

EU targets Temu’s marketplace with €200m fine (📑): The EU penalized the e-commerce giant for failing to stop illegal and unsafe products from spreading across its platform. By targeting algorithmic design as a source of liability, regulators aim to force digital marketplaces to prioritize user safety and ensure that systemic risk assessment is in place.

EU courts fracture Meta’s gatekeeper designation (📑): A mixed DMA ruling upheld Messenger’s status as a gatekeeper but exempted Facebook Marketplace. By assessing individual services rather than interconnected ecosystems, the decision may allow some dominant platforms to protect specific features from blanket regulation.

UK CMA reshapes Google search services to empower publishers (📑): A world-first conduct requirement forces Google to let publishers opt out of having their content power Google Search’s AI features. By curbing unilateral data extraction, the rules may rebalance cross-side bargaining power over content usage.

Platform Papers is published, curated and maintained by Joost Rietveld.