When Delivery Comes to Town

How platform entry affects industry structure and competition

Platform Papers is a blog about platform competition and Big Tech. Prominent academics discuss their latest research. The blog is linked to platformpapers.com, a repository that collects and organizes academic research on platform competition.

Food delivery platforms such as DoorDash and UberEats in the United States, Deliveroo and Just Eat in Europe, and Meituan and GrabFood across Asia have become a defining feature of the modern restaurant industry. For consumers, they promise convenience and variety. For restaurants, they offer access to new customers—along with hefty commissions and new competitive pressures.

So what happens to an industry when these platforms arrive? In a recent paper published in the Strategic Management Journal, we study how the emergence of restaurant delivery platforms reshapes competition and industry structure in the U.S. restaurant sector. Rather than focusing on individual firm performance alone, we ask a broader question: How do digital distribution platforms change who survives, who exits, and how competition works within an industry?

Platforms That Work With Incumbents

Much of what we know about platforms comes from settings like ride-sharing or home-sharing, where platforms introduce new suppliers that compete directly with incumbents. Delivery platforms are different.

Platforms like DoorDash or Grubhub don’t primarily rely on new entrants (at least not initially). Instead, they connect consumers to existing restaurants, acting as strategic intermediaries that facilitate transactions while taking a cut of each order. This could help incumbents by expanding demand and reducing search costs. But it could also intensify competition—both among restaurants, and between restaurants and the platform itself. Which force dominates, and for which types of firms, is not obvious.

A Market-Level View: More Exit, More Concentration

We study the U.S. restaurant industry from 2012 to 2018, a period when delivery platforms rapidly expanded across cities but before ghost kitchens became widespread. Using detailed data on platform penetration and the universe of U.S. restaurants, we first look at what happens at the market level.

Three patterns stand out.

First, restaurant exit increases as delivery platforms penetrate a market. Entry does not rise enough to offset this effect, leading to a decline in business dynamism.

Second, industry concentration increases. As weaker restaurants exit, activity becomes more concentrated among fewer surviving establishments.

Third – and perhaps most striking – we find no evidence that restaurants, as a group, capture more revenue when delivery platforms expand. While consumer demand may grow, the value appears to be captured elsewhere, most plausibly by the platforms themselves.

Together, these results suggest that delivery platforms can disrupt an industry even when they rely on incumbents as partners. These patterns also raise questions not only about firm strategy, but also about how policymakers and platform owners should think about the long-run consequences of platform-mediated competition.

Why Exit Increases: Competition from Two Directions

Why does platform penetration push more restaurants out of business?

Our evidence points to two complementary mechanisms.

Horizontal competition: Delivery platforms reduce the importance of local barriers like geography. A restaurant is no longer competing only with hyper-local establishments, but with a much broader set of alternatives surfaced on a consumer’s phone. In dense restaurant markets, this erosion of barriers makes competition especially intense. In such markets, delivery platforms expand the competitive set and intensify rivalry, increasing exit even when overall consumer demand may be growing.

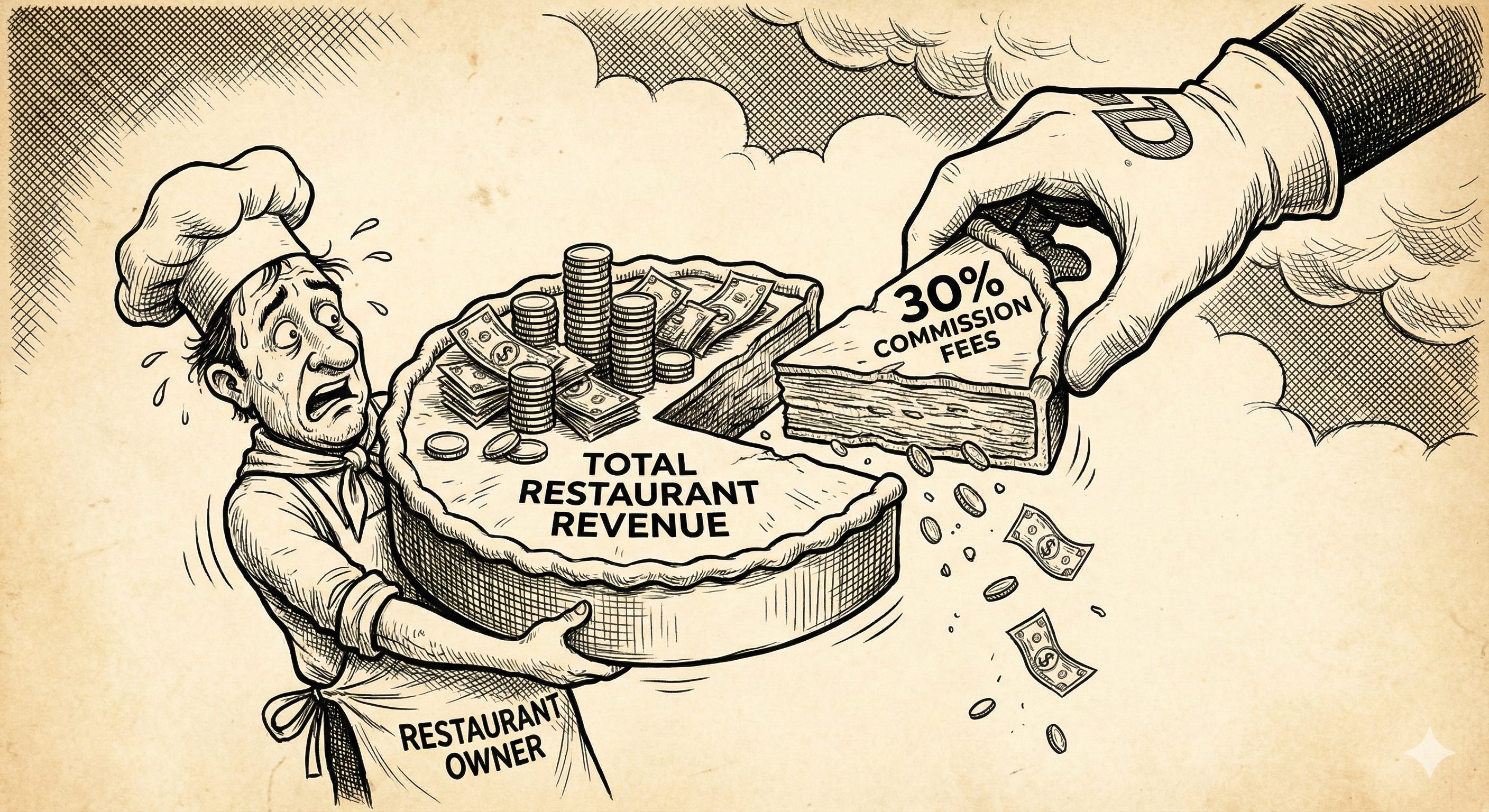

Vertical competition: Platforms don’t just match buyers and sellers – they also extract value. Commissions of 15–30% put pressure on already thin margins. Restaurants that are less operationally efficient appear particularly vulnerable to this margin squeeze. This pushes out less efficient restaurants, even in relatively uncongested markets where horizontal competition should be weakest. This pattern is consistent with vertical competition: when platforms take a share of each transaction, restaurants that lack operational slack are less able to absorb the cost.

Not All Restaurants Are Affected Equally

Our broad results show that platforms can expand access to consumers while also intensifying competition in ways that many incumbents struggle to manage.

The effects of delivery platforms are highly uneven. Restaurants that are operationally efficient—those that can produce more revenue per employee—are better able to withstand platform pressure and cover the platform’s fees. In contrast, low-efficiency restaurants are more likely to exit, suggesting that delivery platforms act as a sorting mechanism, accelerating the exit of establishments that struggle to operate efficiently under tighter margins.

Business models also shape how restaurants experience platform entry. Establishments whose value proposition is tightly linked to in-person consumption (e.g., bars, clubs, and venues oriented around social experiences) are less adversely affected by delivery platforms. That their core offering does not translate easily into delivery may even mean that delivery platforms help these firms stay in business, as consumers shift spending from “eating out” to “spending time out with friends.” By contrast, restaurants whose offerings are naturally suited to delivery (e.g., quick-service or takeout-oriented cuisines) face more intense competition. These establishments are more directly exposed to platform-mediated comparison, where consumers can easily substitute between similar options with a few taps on a screen.

More broadly, delivery platforms revalue restaurant assets and capabilities. Characteristics that once conferred advantage—such as prime location or walkable foot traffic—become less important when demand is routed through a digital intermediary. In our data, this revaluation is visible in the diminished protective effect of location-based accessibility as platform penetration increases.

Taken together, these patterns suggest that delivery platforms do not simply raise or lower the tide for all restaurants. Instead, they reshape the basis of competition, favoring some business models and capabilities while accelerating exit for others.

About The Research: We study the emergence of four leading food delivery platforms in the U.S. (2012-2018). Combining consumer-level, credit card-based data on platform adoption across 924 U.S. metropolitan areas with establishment-level data covering over 750,000 restaurants, we analyze how increased delivery platform penetration in a metro area relates to market and firm outcomes. Market-level panel regressions show that greater platform penetration is associated with higher restaurant exit, lower business dynamism, and increased industry concentration, with no increase in restaurant revenue. Firm-level survival regressions show that exit increases most for operationally inefficient restaurants and those in restaurant-dense markets, consistent with intensified vertical competition from platform fees and horizontal competition from expanded competitive sets.

Implications for Policy and Platform Strategy

Our findings also speak directly to ongoing policy debates around digital platforms, as delivery platforms highlight a tension that regulators increasingly face. On the one hand, platforms clearly benefit consumers by increasing convenience, variety, and access. On the other hand, our results suggest that these benefits may come alongside higher exit, lower business dynamism, and greater concentration among incumbent providers.

This raises an important distinction: even if platforms improve consumer welfare in the short run, they may still reshape markets in ways that concern policymakers focused on competition, small business survival, and local economic vitality. In the restaurant industry, delivery platforms appear to accelerate consolidation, disproportionately affecting smaller, younger, and less efficient establishments. These effects may be especially salient for local economies that rely on independent restaurants as sources of employment and neighborhood identity.

Importantly, our results do not imply that platforms are “bad” or that their growth should necessarily be restricted. Rather, they suggest that platform regulation needs to account for indirect and long-run effects on market structure, not just prices or output. Policies that focus narrowly on consumer outcomes may miss how value is redistributed away from producers and how competitive pressure is amplified through platform-mediated markets.

Our findings also have implications for platform owners themselves. Delivery platforms depend on a healthy ecosystem of restaurants to generate value. Yet the same mechanisms that fuel platform growth (reduced search frictions, expanded competitive sets, and commission-based monetization) can increase exit among the very businesses the platform relies on. In the long run, this creates a strategic tradeoff: platforms may grow faster by intensifying competition and extracting value, but doing so risks hollowing out the supply side of the market.

From this perspective, platform owners face an ecosystem management problem rather than a simple growth problem. Sustaining long-run value creation may require balancing short-term monetization against the viability of complementors, for example through differentiated pricing, operational support, or tools that help restaurants adapt rather than simply compete on the platform.

Implications Beyond Restaurants

While our study focuses on food delivery, the implications extend beyond restaurants. Similar digital distribution platforms now operate in groceries, retail, health services, and professional services.

For managers, the message is not simply to embrace or reject platforms, but to understand how platforms reshape competition—and whether their business model fits the new rules of the game. For researchers and policymakers, the results underscore that platforms can drive consolidation and exit even when they partner with incumbents, raising important questions about market structure, value capture, and long-run industry health.

Delivery platforms may make life easier for consumers. But when they come to town, they also quietly—and profoundly—reshape the competitive landscape.

This post is based on research published in the Strategic Management Journal and is included in the Platform Papers references dashboard:

Raj, M., & Eggers, J. P. (2025). When delivery comes to town: The effect of digital distribution platform emergence on industry structure and competition. Strategic Management Journal.

Podcast Tip: Talking about Platforms

Our friends from Talking about Platforms bring the latest discoveries from the field of platform research right into your preferred podcasting app. Talking About Platforms is a podcast where hosts Philip, Daniel, and Tommaso make sense of the underlying mechanisms that have enabled and facilitated the rise of digital platforms.

Listen to latest episode here, or subscribe wherever you get your podcasts.

Platform Updates

For more on delivery platforms, see The Hidden Cost of Platform Diversification, on the effects of Uber expanding into food delivery on its ride-sharing business, and Regulating Powerful Platforms, on how regulating food-delivery platforms had unintended consequences for restaurants.

Mamdani makes delivery apps pay up - New York struck a $5.2 million deal with Uber Eats, Fantuan, and HungryPanda for underpaying nearly 50,000 couriers, while Uber must reinstate up to 10,000 deactivated workers. The city is turning gig‑platform pay, tipping, and deactivation tricks into regulatory enforcement cases.

Microsoft’s AI bet spooks Wall Street - Microsoft beat Q2 expectations with $81.3B revenue and strong Azure growth, but a $37.5B capex surge—up 66% for AI data centers—tanked the stock. Investors fear the hyperscale infrastructure race won’t monetize fast enough to justify the massive OpenAI-fueled spend.

Xbox platform future in doubt - Xbox revenue fell 9% last quarter, hardware sales dropped 32%, raising concerns that Game Pass and cross-platform bets may not be enough to offset a weakened console base. Microsoft seems to risk becoming just a mega-publisher as its hardware may shrink to a niche, PC-like device or vanish entirely.

Amazon retreats from brick‑and‑mortar grocery - Amazon is shutting all 57 Fresh supermarkets and 15 Go stores after they failed to stand out, shifting investment to online grocery and a Whole Foods network. The move doubles down on same‑day delivery and high‑margin platform plays while repurposing “Just Walk Out” tech as a licensable business.

Google pays for data grabs, keeps the data machine - Google will pay over $200 million to settle claims that Android quietly siphoned mobile data and that Google Assistant secretly recorded private chats for ads. Ambient telemetry and always‑on assistants seem to remain core to Google’s business model of data-hungry personalization.

Apple rides iPhone boom while renting its AI - Record iPhone 17 sales gave Apple its strongest growth since 2021, even as Mac and wearable revenue slipped. Apple is keeping capex lean and partnering with Google’s Gemini for Siri and Apple Intelligence—doubling down on premium hardware while outsourcing the heaviest AI lift.

TikTok cuts a US survival deal - New US joint venture with Oracle licensing the algorithm keeps TikTok (plus CapCut, Lemon8) running, while ByteDance retains a 19.9% stake. Users get “same app, same account” continuity, but expect US‑governed feeds that gradually prioritize US content over TikTok’s global mix.

Platform Papers is published, curated and maintained by Joost Rietveld.